Understanding the FSBO Transaction Process (Step-by-Step Guide)

Once you accept an offer on your home, you enter the transaction phase, the part of the process where everything becomes official.

This is also where many FSBO sellers feel the most uncertainty.

What happens next?

Who does what?

What could go wrong?

If you understand the steps ahead of time, you can move through the transaction with confidence and avoid the most common pitfalls.

Why Understanding the Transaction Process Matters

The transaction phase is where deals are either completed or fall apart.

Most Problems Happen After the Offer Is Accepted

Common issues include:

- Inspection disputes

- Appraisal problems

- Financing delays

- Miscommunication

Preparation Reduces Risk

When you know what’s coming, you can:

- Respond quickly

- Make better decisions

- Keep the deal on track

👉 Read next: How To Sell Your Home FSBO (Complete Guide)

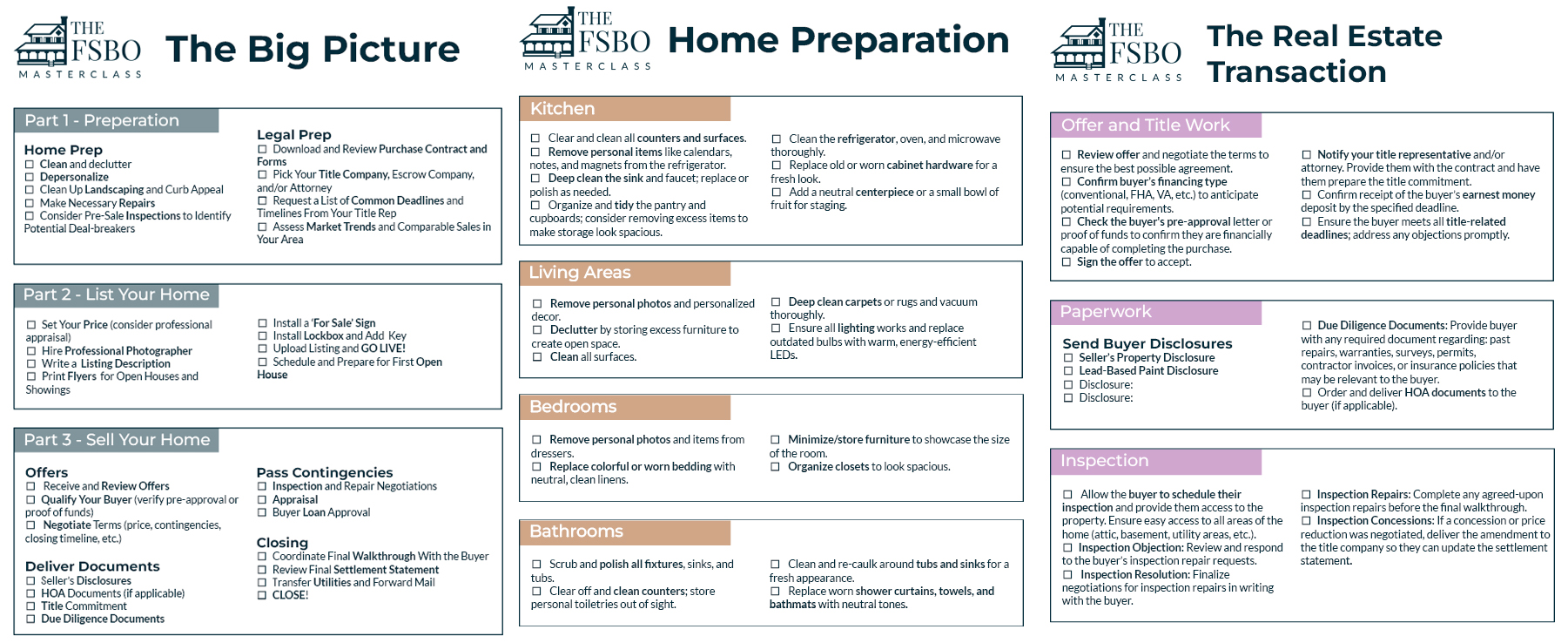

Step 1: Finalize the Contract

Once you accept an offer, both parties sign the purchase agreement.

What This Means

- The deal becomes legally binding

- Deadlines are established

- Responsibilities are defined

What to Double-Check

- Purchase price

- Contingencies

- Timeline

- Inclusions/exclusions (appliances or personal items in the contract)

👉 Read next: Understanding the Purchase Agreement (FSBO Guide)

Step 2: Earnest Money Deposit

The buyer submits earnest money shortly after going under contract.

What Is Earnest Money?

A deposit that shows the buyer is serious (literally earnest).

Why It Matters

- Protects you if the buyer backs out improperly (non-contractually)

- Signals commitment

Typical Amount

Often 1%–3% of the purchase price (varies by market).

👉 Read next: What Contingencies Mean in Real Estate (And Why They Matter)

Step 3: The Home Inspection

Most buyers will conduct an inspection.

What Happens During Inspection

- An inspector evaluates the home

- The buyer receives a report

- Issues are identified

What Comes Next

The buyer may:

- Request repairs

- Ask for a credit

- Accept the home as-is

Your Options

You can:

- Agree

- Negotiate

- Decline

PRO TIP

Buyer concerns can be addressed by combining repairs with financial concessions. For example, you have a plumber fix a leaking sink, but you offer a small financial concession to alleviate a buyer's concerns about an older but functioning water heater.

👉 Read next: The Home Inspection Process Explained for FSBO Sellers

Step 4: The Appraisal

If the buyer is using a loan, the lender will most likely require an appraisal.

What the Appraisal Does

Determines whether the home value supports the loan amount.

Possible Outcomes

Appraisal Meets Value

No issue and the deal continues.

Appraisal Comes in Low

You may need to:

- Lower the price

- Renegotiate or risk losing the deal

Depending on the market, a buyer may be willing to pay cash to cover the “appraisal gap”. However, most of the time a seller is expected to lower the purchase price to meet the appraised value.

Appraisal Comes in High

The buyer does not need to tell you the exact value, and the deal continues.

👉 Read next: What Happens If the Appraisal Comes in Low? (FSBO Guide)

Step 5: Loan Approval (If Applicable)

If the buyer is financing, their lender will finalize the loan.

What This Includes

- Income verification

- Credit review

- Final approval

Potential Delays

- Missing documents

- Changes in buyer’s financial situation

PRO TIP

Stay in communication with the buyer, their agent, or their lender to ensure progress is on track.

👉 Read next: What Happens After You Accept an Offer? (FSBO Step-by-Step Guide)

Step 6: Title and Closing Preparation

A title company or attorney typically handles this stage.

What Happens Here

- Title search

- Title insurance preparation

- Closing documents prepared

Why This Matters

Ensures:

- Clean ownership transfer

- No unexpected claims

PRO TIP

Depending on your state you are likely paying an attorney or title company. Ask them questions.

👉 Read next: Do FSBO Sellers Need a Title Company or Attorney? (FSBO Guide)

Step 7: Final Walkthrough

Before closing, the buyer will typically do a final walkthrough.

Purpose

To confirm:

- The home is in agreed condition

- Repairs (if any) are completed

- No new issues have arisen

What You Should Do

- Leave the home clean

- Ensure agreed repairs are done

- Typically the seller has removed personal belongings and is moved out of the home

👉 Read Next: How to Price Your Home Without a Realtor (FSBO Pricing Guide)

Step 8: Closing Day

This is when the sale is finalized.

What Happens at Closing

- Documents are signed

- Funds are transferred

- Ownership changes hands

What You’ll Need

- Identification

- Required documents

- Access instructions (keys, garage remotes, etc.)

After Closing

- Funds are disbursed

- The transaction is complete

👉 Read next: What Happens at Closing? (FSBO Step-by-Step Guide)

Common FSBO Transaction Problems

Inspection Negotiation Issues

Disagreements over repairs can delay or kill deals.

Low Appraisal

A common issue in competitive markets where buyers bid above the asking price.

Financing Delays

Can push closing timelines.

Poor Communication

Miscommunication can create unnecessary problems.

👉 Read next: Common Mistakes FSBO Sellers Make During the Transaction

Pro Tips From a Real Estate Professional

Stay Organized

Track deadlines and documents carefully.

Communicate Clearly

Keep all parties informed.

Be Flexible (When Reasonable)

Small contract adjustments or concessions can keep deals alive.

Anticipate Issues

Understanding common problems helps you prepare.

👉 Read Next: How to Prepare Your Home for Sale By Owner

Frequently Asked Questions

How long does the transaction process take?

Typically 30–45 days, depending on financing and contingencies and your state.

Who manages the transaction in FSBO?

You do, but title companies, attorneys, and lenders are also involved.

Do I need a title company?

In most states, yes.

Can a deal fall apart after going under contract?

Yes. Inspection, appraisal, and financing issues are common causes.

👉 Read Next: How to Market a FSBO Property (Complete Guide)

Final Thoughts

The FSBO transaction process may seem complicated, but it’s actually very structured.

When you understand:

- What happens at each step

- What to expect

- Where issues can arise

…you can navigate the process confidently and keep your sale on track.

👉 Read Next: How to Handle Offers Without a Realtor (FSBO Guide)

Download Your FSBO Transaction Checklist

To keep FSBO sellers on top of their transactions I created a FREE checklist.